Stop! Before you sign those loan papers, discover why a ₹1 Lakh down payment is the smartest move for the 2026 Tata Punch. Learn the “5-Year Sweet Spot” trick that saves you over ₹50,000 in interest and see the exact EMI breakdown you won’t find at the dealership.

So, you’re eyeing the 2026 Tata Punch Facelift – a smart choice for its safety, new Turbo engine, and robust design. But beyond the excitement of a new car, the biggest question often is: “How much will it really cost me every month?”

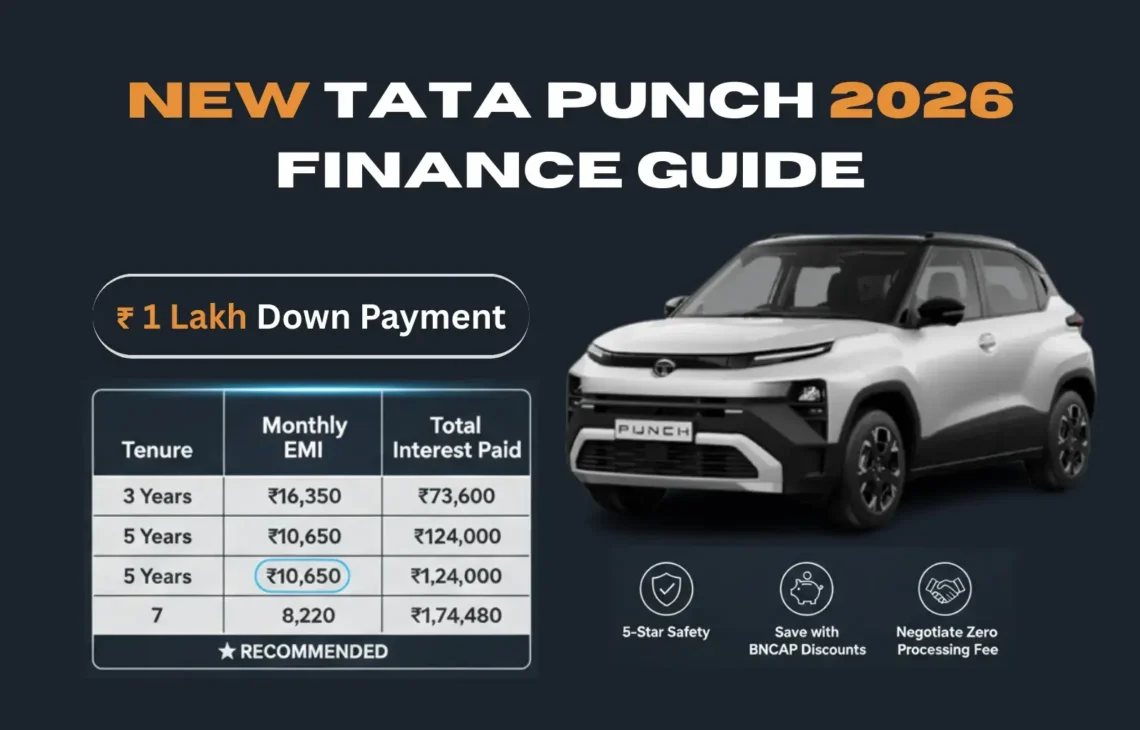

You’re planning a ₹1 Lakh down payment, which is a solid start. Let’s break down the actual costs, calculate your EMIs, and arm you with expert financial advice to make your Tata Punch purchase as smooth and affordable as possible.

First, The On-Road Price: More Than Just Ex-Showroom!

Many first-time buyers mistakenly calculate their EMI based on the ex-showroom price. However, the true cost includes mandatory charges like RTO (Road Tax & Registration), Insurance, and FastTag.

For the 2026 Tata Punch Smart (Base Model) with an ex-showroom price of ₹5,59,000, here’s an estimated on-road price (this can vary slightly by city and state):

- Ex-Showroom Price: ₹5,59,000

- Road Tax & Registration (RTO): ₹40,000 – ₹45,000 (approx. 7-8% of ex-showroom)

- Insurance (1st Year Comprehensive): ₹12,000 – ₹15,000

- FastTag & Other Charges: ₹500 – ₹1,000

- Estimated On-Road Price: ₹6,11,500 – ₹6,20,000

With your ₹1,00,000 down payment, your total loan amount will be approximately ₹5,11,500 – ₹5,20,000. For our calculations, we’ll use an average loan amount of ₹5,15,000.

Your Monthly EMI Breakdown: The Numbers You Need

Assuming a car loan interest rate of 8.75% per annum (a good average for individuals with a credit score of 750+ in January 2026):

| Loan Tenure | Total Loan Amount (Approx.) | Monthly EMI (Approx.) | Total Interest Paid |

| 3 Years (36 Months) | ₹5,15,000 | ₹16,350 | ₹73,600 |

| 5 Years (60 Months) | ₹5,15,000 | ₹10,650 | ₹1,24,000 |

| 7 Years (84 Months) | ₹5,15,000 | ₹8,220 | ₹1,74,480 |

Expert Financial Advice: Save Thousands on Your Tata Punch Loan!

Beyond the EMI, an expert finance advisor can help you trim down costs and navigate the loan process smartly.

The “5-Year Sweet Spot”

While a 7-year EMI of ₹8,220 looks low, you end up paying an additional ₹50,000 in interest compared to a 5-year loan. My advice? Opt for the 5-year tenure (₹10,650 EMI) if your budget allows. It balances affordability with minimizing total interest outflow.

Harness the Power of a Good CIBIL Score

A credit score above 750 is your biggest asset. It qualifies you for the best interest rates (like the 8.75% used above), saving you thousands over the loan period. If your score is lower, work on improving it before applying for the loan.

You May read Also: How to Improve Your Credit Score Fast: The Ultimate Guide to Financial Credibility

Negotiate on Insurance

Never simply accept the insurance quote from the dealership. As the Punch secured a 5-star Bharat NCAP rating, many insurers offer safety discounts. Get at least 2-3 quotes from independent online aggregators (e.g., PolicyBazaar, Coverfox) and use them to negotiate a better deal with the dealer’s insurer. This can save you ₹1,000 – ₹3,000 upfront.

Beware of “Hidden” Loan Processing Fees

Banks often charge a processing fee (0.5% – 1% of the loan amount). During festive seasons or high-volume sales months (like January), banks might waive this. Always negotiate for a zero processing fee to save ₹2,500 – ₹5,000 immediately.

Consider a Higher Down Payment

If you can stretch your down payment to ₹1.5 Lakhs or even ₹2 Lakhs, your EMI will drop significantly, and so will your total interest burden. Even an extra ₹50,000 upfront can shave off a few hundred rupees from your monthly EMI and substantially reduce the total interest paid.

The Balloon EMI Scheme (New in 2026)

Ask your Tata Motors dealer about “Balloon Financing” or “Step-Up EMIs.” Some banks (like Tata Capital or HDFC Bank) now offer schemes where your initial EMIs are significantly lower (e.g., ₹5,999 for the first 2-3 years), with a larger “bullet payment” due at the end of the loan tenure. This can ease your initial financial burden but be prepared for the final payment.

Pro Tip: Always read the fine print!

Is Your Budget Ready for the Tata Punch?

Based on our calculations, if your household’s net monthly income is comfortably above ₹30,000 – ₹35,000, an EMI of around ₹10,650 for 5 years should be manageable, allowing you to enjoy your new Tata Punch without financial strain. Remember to factor in fuel costs (approx. ₹3,000-₹5,000/month for average usage) and occasional maintenance.

The 2026 Tata Punch is a phenomenal package, especially with its safety and new features. By following these expert financial tips, you can ensure your purchase is not just exciting, but also financially sound.